A journal of IEEE and CAA , publishes

high-quality papers in English on original

theoretical/experimental research

and development in all areas of automation

Volume 11

Issue 3

Volume 11

Issue 3

IEEE/CAA Journal of Automatica Sinica

| Citation: | P. Huang, G. Wang, S. Wang, and H. Xiao, “A mean-field game for a forward-backward stochastic system with partial observation and common noise,” IEEE/CAA J. Autom. Sinica, vol. 11, no. 3, pp. 746–759, Mar. 2024. doi: 10.1109/JAS.2023.124047

|

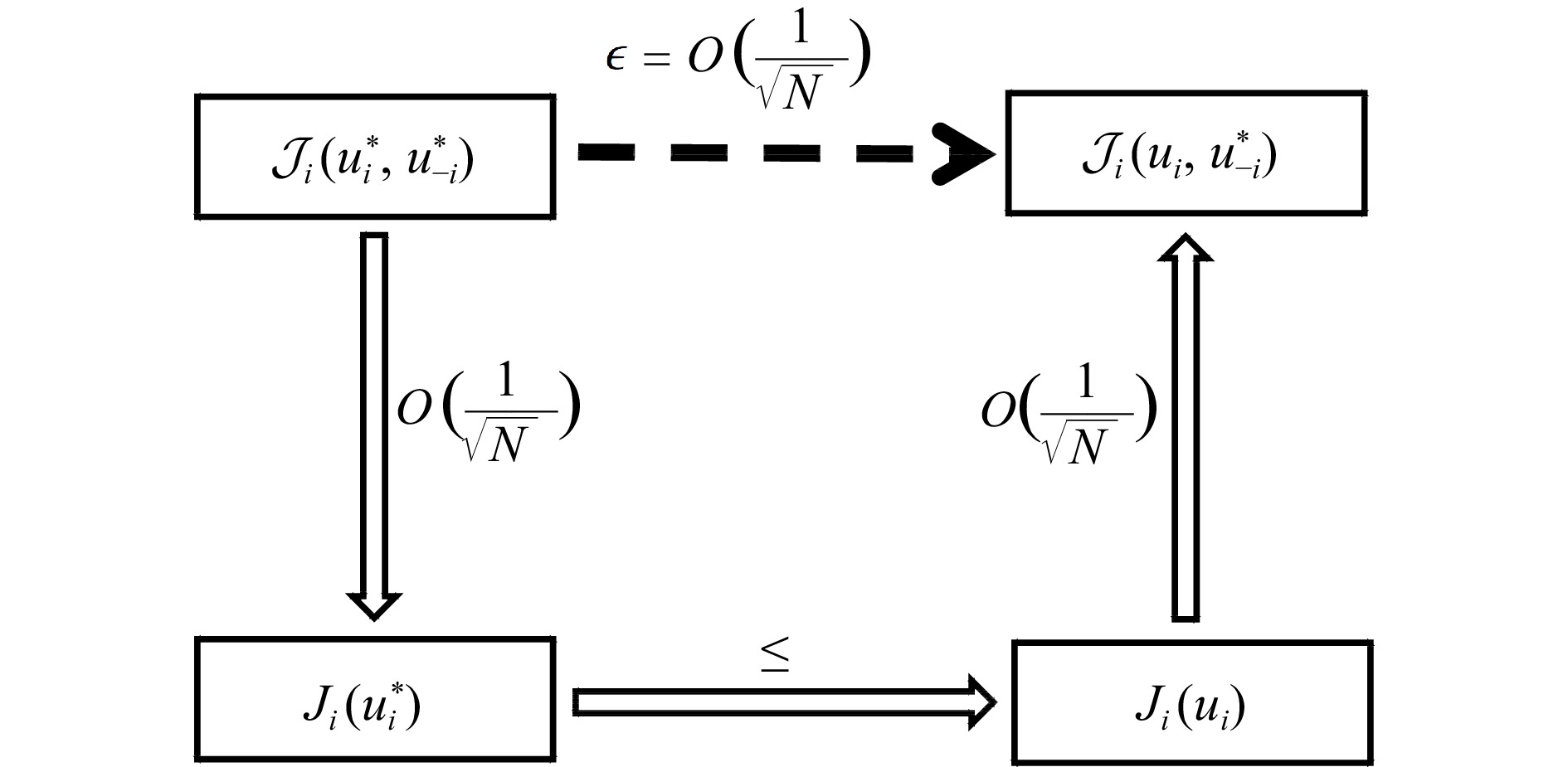

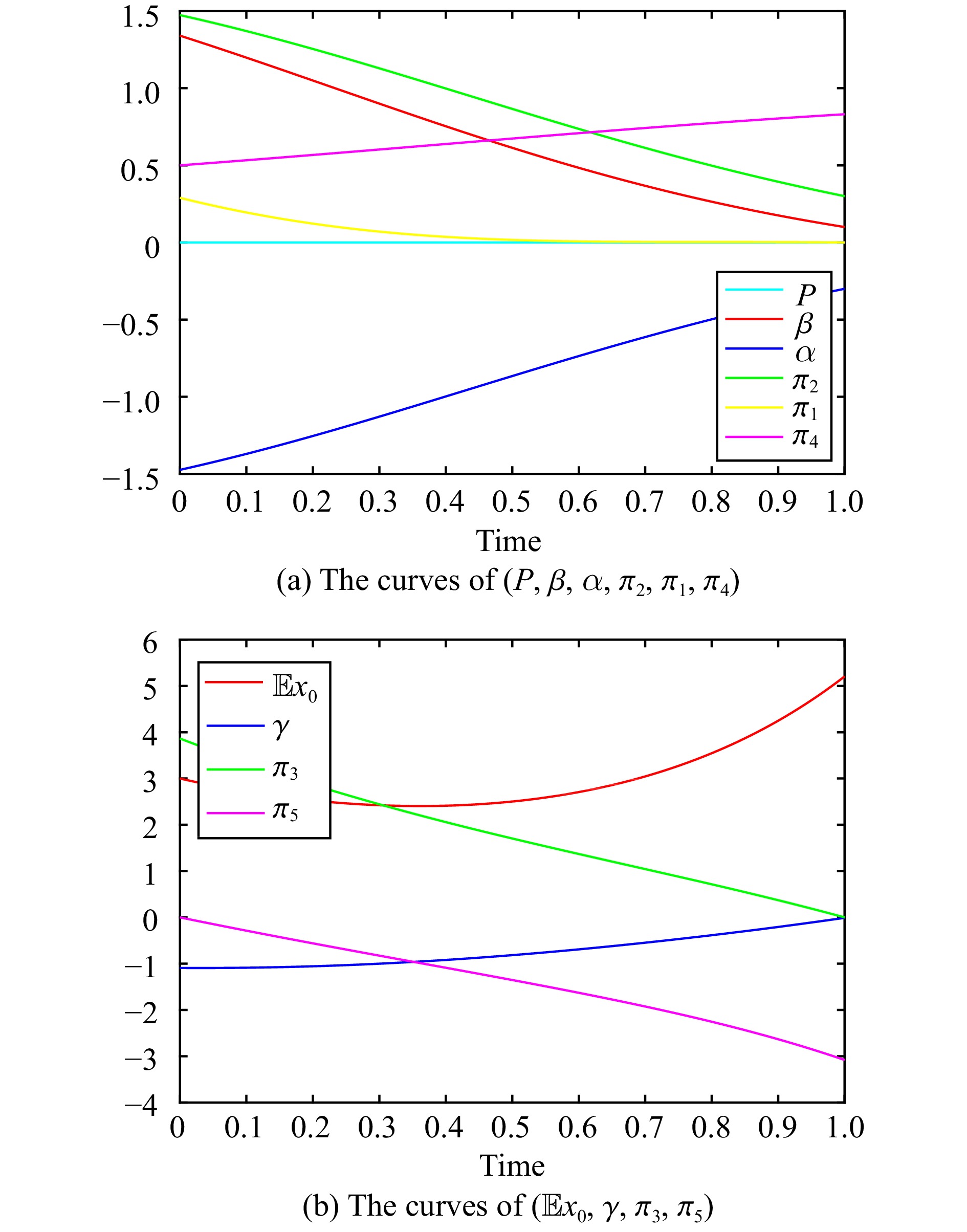

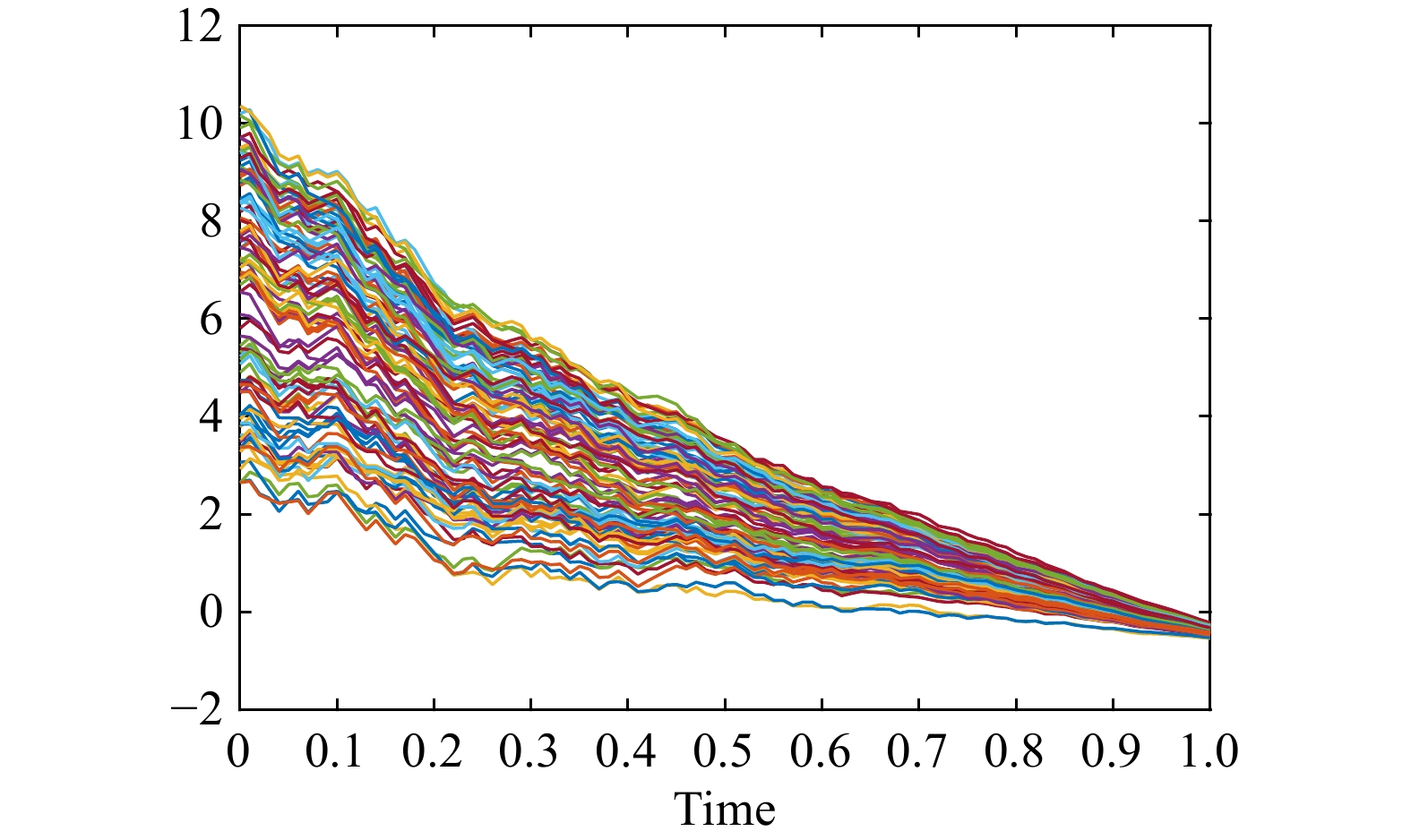

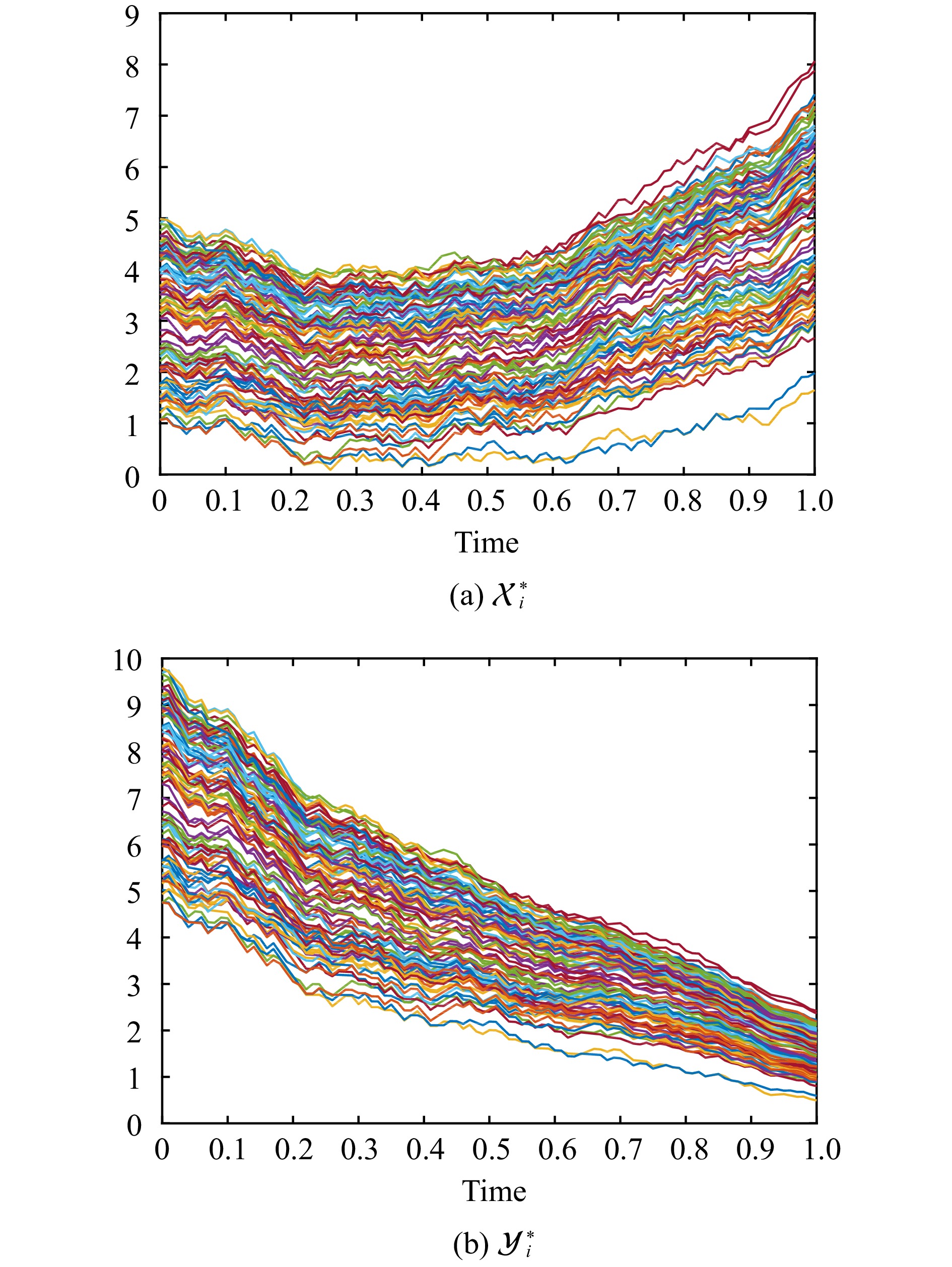

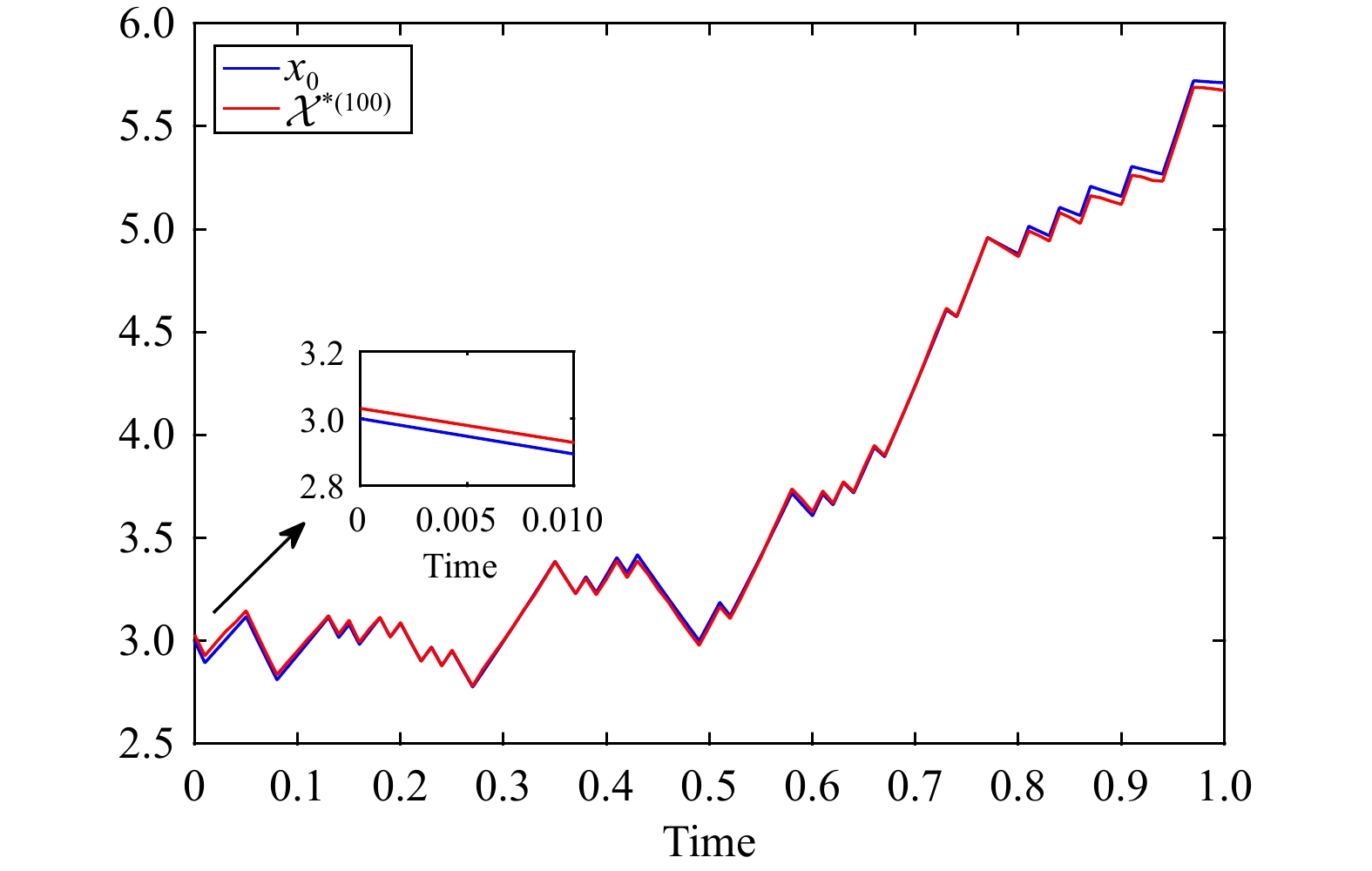

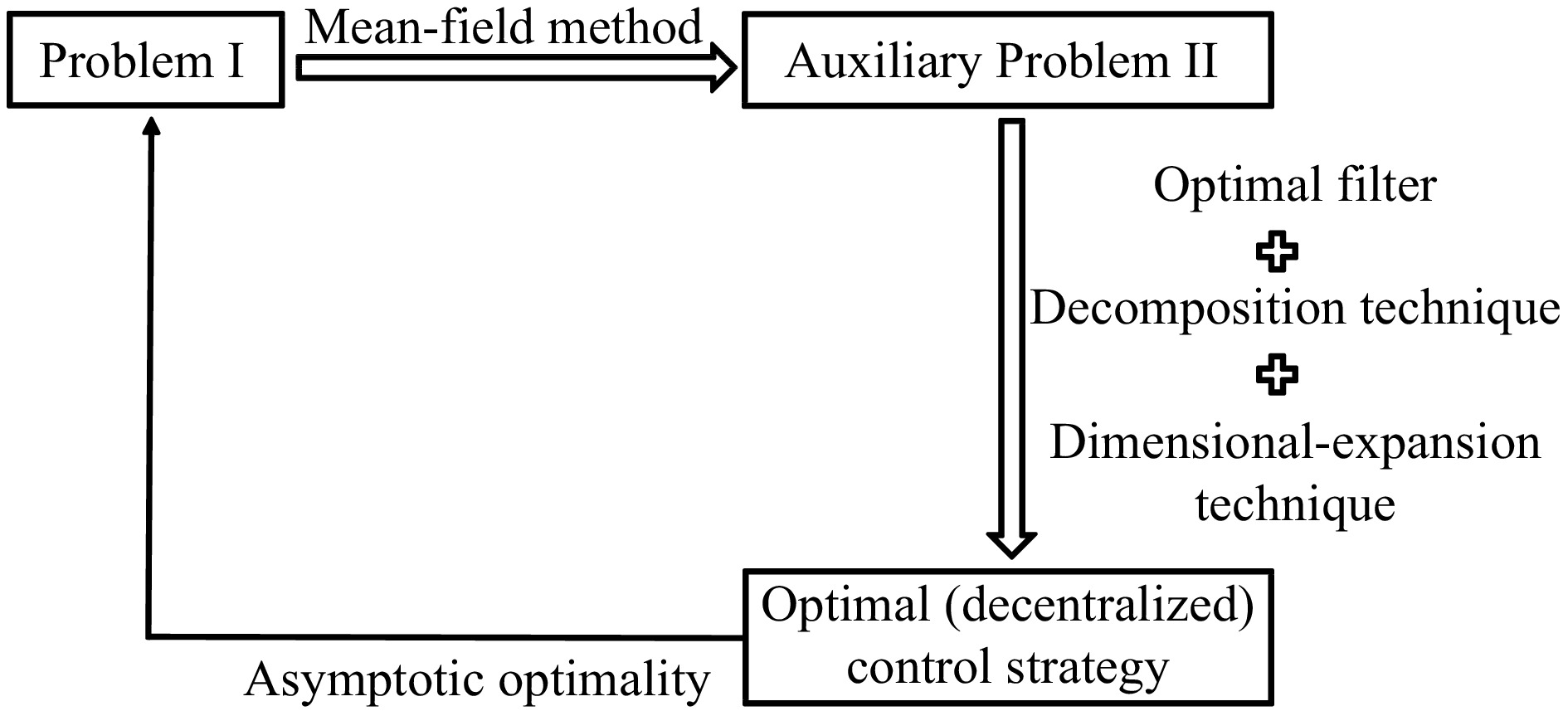

This paper considers a linear-quadratic (LQ) mean-field game governed by a forward-backward stochastic system with partial observation and common noise, where a coupling structure enters state equations, cost functionals and observation equations. Firstly, to reduce the complexity of solving the mean-field game, a limiting control problem is introduced. By virtue of the decomposition approach, an admissible control set is proposed. Applying a filter technique and dimensional-expansion technique, a decentralized control strategy and a consistency condition system are derived, and the related solvability is also addressed. Secondly, we discuss an approximate Nash equilibrium property of the decentralized control strategy. Finally, we work out a financial problem with some numerical simulations.

| [1] |

J. M. Lasry and P. L. Lions, “Mean field games,” Jpn. J. Math., vol. 2, pp. 229–260, Mar. 2007. doi: 10.1007/s11537-007-0657-8

|

| [2] |

M. Huang, P. E. Caines, and R. P. Malhamé, “Large-population cost-coupled LQG problems with non-uniform agents: Individual-mass behavior and decentralized ε-Nash equilibria,” IEEE Trans. Autom. Control, vol. 52, pp. 1560–1571, Sept. 2007. doi: 10.1109/TAC.2007.904450

|

| [3] |

R. Carmona, F. Delarue, and D. Lacker, “Mean field games with common noise,” Ann. Probab., vol. 44, no. 6, pp. 3740–3803, 2016.

|

| [4] |

A. Aurell, R. Carmona, G. Dayanikli, and M. Lauriere, “Optimal incentives to mitigate epidemics: A Stackelberg mean field game approach,” SIAM J. Control Optim., vol. 60, no. 2, pp. 294–322, Apr. 2022. doi: 10.1137/20M1377862

|

| [5] |

J. Moon and T. Bașar, “Linear quadratic mean field Stackelberg differential games,” Automatica, vol. 97, pp. 200–213, Dec. 2018. doi: 10.1016/j.automatica.2018.08.008

|

| [6] |

A. Bensoussan, K. C. Sung, S. C. Yam, and S. P. Yung, “Linear-quadratic mean field games,” J. Optim. Theory Appl., vol. 169, no. 2, pp. 496–529, 2016. doi: 10.1007/s10957-015-0819-4

|

| [7] |

J. Moon and T. Bașar, “Linear quadratic risk-sensitive and robust mean field games,” IEEE Trans. Autom. Control, vol. 62, no. 3, pp. 1062–1077, Mar. 2017. doi: 10.1109/TAC.2016.2579264

|

| [8] |

R. Xu and F. Zhang, “ϵ-Nash mean-field games for general linear-quadratic systems with applications,” Automatica, vol. 114, p. 108835, Jan. 2020.

|

| [9] |

M. Li, N. Li, and Z. Wu, “Linear-quadratic mean-field game for stochastic large-population systems with jump diffusion,” IET Control Theory Appl., vol. 14, no. 3, pp. 481–489, Feb. 2020. doi: 10.1049/iet-cta.2019.0270

|

| [10] |

B. Wang and J. Zhang, “Distributed output feedback control of Markov jump multi-agent systems,” Automatica, vol. 49, no. 5, pp. 1397–1402, May 2013. doi: 10.1016/j.automatica.2013.01.063

|

| [11] |

Y. Xu, Y. Yuan, Z. Wang, and X. Li, “Noncooperative model predictive game with Markov jump graph,” IEEE/CAA J. Autom. Sinica, vol. 10, no. 4, pp. 1–14, Apr. 2022.

|

| [12] |

Y. Achdou, P. Mannucci, C. Marchi, and N. Tchou, “Deterministic mean field games with control on the acceleration and state constraints,” SIAM J. Math. Anal., vol. 54, no. 3, pp. 3757–3788, Jun. 2022. doi: 10.1137/21M1415492

|

| [13] |

Y. Hu, J. Huang, and T. Nie, “Linear-quadratic-Gaussian mixed mean-field games with heterogeneous input constraints,” SIAM J. Control Optim., vol. 56, no. 4, pp. 2835–2877, 2018. doi: 10.1137/17M1151420

|

| [14] |

J. F. Bonnans, J. Gianatti, and L. Pfeiffer, “A Lagrangian approach for aggregative mean field games of controls with mixed and final constraints,” SIAM J. Control Optim., vol. 61, no. 1, pp. 105–134, Feb. 2023. doi: 10.1137/21M1407720

|

| [15] |

M. Huang, P. Caines, and R. Malhamé, “Social optima in mean field LQG control: Centralized and decentralized strategies,” IEEE Trans. Autom. Control, vol. 57, no. 7, pp. 1736–1751, Jul. 2012. doi: 10.1109/TAC.2012.2183439

|

| [16] |

B. Wang, H. Zhang, and J. Zhang, “Mean field linear quadratic control: Uniform stabilization and social optimality,” Automatica, vol. 121, pp. 1–14, Nov. 2020.

|

| [17] |

K. Du, J. Huang, and Z. Wu, “Linear quadratic mean-field-game of backward stochastic differential systems,” Math. Control Relat. Fields, vol. 8, pp. 653–678, 2018. doi: 10.3934/mcrf.2018028

|

| [18] |

J. Huang, S. Wang, and Z. Wu, “Backward mean-field linear-quadratic-Gaussian (LQG) games: Full and partial information,” IEEE Trans. Autom. Control, vol. 61, no. 12, pp. 3784–3796, Dec. 2016. doi: 10.1109/TAC.2016.2519501

|

| [19] |

M. Ye, D. Li, Q.-L. Han, and L. Ding, “Distributed Nash equilibrium seeking for general networked games with bounded disturbances,” IEEE/CAA J. Autom. Sinica, vol. 10, no. 2, pp. 376–387, Feb. 2023. doi: 10.1109/JAS.2022.105428

|

| [20] |

B. Djehiche, H. Tembine, and R. Tempone, “A stochastic maximum principle for risk-sensitive mean-field type control,” IEEE Trans. Autom. Control, vol. 60, no. 10, pp. 2640–2649, Feb. 2015. doi: 10.1109/TAC.2015.2406973

|

| [21] |

M. Hafayed and S. Meherrem, “On optimal control of mean-field stochastic systems driven by Teugels martingales via derivative with respect to measures,” Internat. J. Control, vol. 93, no. 5, pp. 1053–1062, 2020. doi: 10.1080/00207179.2018.1489148

|

| [22] |

Y. Ni, J. Zhang, and M. Krstic, “Time-inconsistent mean-field stochastic LQ problem: Open-loop time-consistent control,” IEEE Trans. Autom. Control, vol. 63, no. 9, pp. 2771–2786, Sept. 2018. doi: 10.1109/TAC.2017.2776740

|

| [23] |

B. Yang and J. Wu, “Infinite horizon optimal control for mean-field stochastic delay systems driven by Teugels martingales under partial information,” Optim. Control Appl. Meth., vol. 41, pp. 1371–1397, 2020. doi: 10.1002/oca.2602

|

| [24] |

J. Yong, “A linear-quadratic optimal control problem for mean-field stochastic differential equations,” SIAM J. Control Optim., vol. 51, no. 4, pp. 2809–2838, 2013. doi: 10.1137/120892477

|

| [25] |

H. Wang, C. Zhang, K. Li, and X. Ma, “Game theory-based multi-agent capacity optimization for integrated energy systems with compressed air energy storage,” Energy, vol. 221, p. 119777, Apr. 2021.

|

| [26] |

S. Wu, “Partially-observed maximum principle for backward stochastic differential delay equations,” IEEE/CAA J. Autom. Sinica, pp. 1–6, Mar. 2017. DOI: 10.1109/JAS.2017.7510472.

|

| [27] |

H. Ma and B. Liu, “Linear-quadratic optimal control problem for partially observed forward-backward stochastic differential equations of mean-field type,” Asian J. Control, vol. 18, no. 6, pp. 2146–2157, May 2016. doi: 10.1002/asjc.1310

|

| [28] |

M. Wang, Q. Shi, and Q. Meng, “Optimal control of forward-backward stochastic jump-diffusion differential systems with observation noises: Stochastic maximum principle,” Asian J. Control, vol. 23, no. 1, pp. 241–254, 2021. doi: 10.1002/asjc.2272

|

| [29] |

Y. Wang and L. Wang, “Forward-backward stochastic differential games for optimal investment and dividend problem of an insurer under model uncertainty,” Appl. Math. Model., vol. 58, pp. 254–269, Jun. 2018. doi: 10.1016/j.apm.2017.07.027

|

| [30] |

S. Zhang, J. Xiong, and X. Liu, “Stochastic maximum principle for partially observed forward-backward stochastic differential equations with jumps and regime switching,” Sci. China Inf. Sci., vol. 61, no. 7, p. 070211, Jul. 2018. doi: 10.1007/s11432-017-9267-0

|

| [31] |

S. Wang and H. Xiao, “Individual and mass behavior in large population forward-backward stochastic control problems: Centralized and Nash equilibrium solutions,” Optim. Control Appl. Meth., vol. 42, pp. 1269–1292, Apr. 2021. doi: 10.1002/oca.2727

|

| [32] |

A. Bensoussan, X. Feng, and J. Huang, “Linear-quadratic-Gaussian mean-field-game with partial observation and common noise,” Math. Control Relat. Fields, vol. 11, no. 1, pp. 23–46, 2021. doi: 10.3934/mcrf.2020025

|

| [33] |

P. Huang, G. Wang, W. Wang, and Y. Wang, “A linear-quadratic mean-field game of backward stochastic differential equation with partial information and common noise,” Appl. Math. Comput., vol. 446, p. 127899, 2023.

|

| [34] |

G. Wang, Z. Wu, and J. Xiong, “A linear-quadratic optimal control problem of forward-backward stochastic differential equations with partial information,” IEEE Trans. Autom. Control, vol. 60, no. 11, pp. 2904–2916, Nov. 2015. doi: 10.1109/TAC.2015.2411871

|

| [35] |

G. Wang, Z. Wu, and J. Xiong, An Introduction to Optimal Control of FBSDE With Incomplete Information. New York: Springer-Verlag, 2018.

|

| [36] |

A. E. B. Lim and X. Zhou, “Linear-quadratic control of backward stochatic differential equations,” SIAM J. Control Optim., vol. 40, no. 2, pp. 450–474, 2001. doi: 10.1137/S0363012900374737

|

| [37] |

E. Pardoux, and S. Peng, “Adapted solution of backward stochastic equation,” Systems Control Lett., vol. 14, no. 1, pp. 55–61, Jan. 1990. doi: 10.1016/0167-6911(90)90082-6

|

| [38] |

D. Majerek, W. Nowak, and W. Zieba, “Conditional strong law of large number,” Int. J. Pure Appl. Math., vol. 20, no. 2, pp. 143–156, 2005.

|

| [39] |

J. Engwerda, LQ Dynamic Optimization and Differential Games. Chichester, West Sussex, England: John Wiley and Sons Ltd, 2005.

|

Figures(6)

DownLoad:

DownLoad: