A journal of IEEE and CAA , publishes

high-quality papers in English on original

theoretical/experimental research

and development in all areas of automation

Volume 7

Issue 3

Volume 7

Issue 3

IEEE/CAA Journal of Automatica Sinica

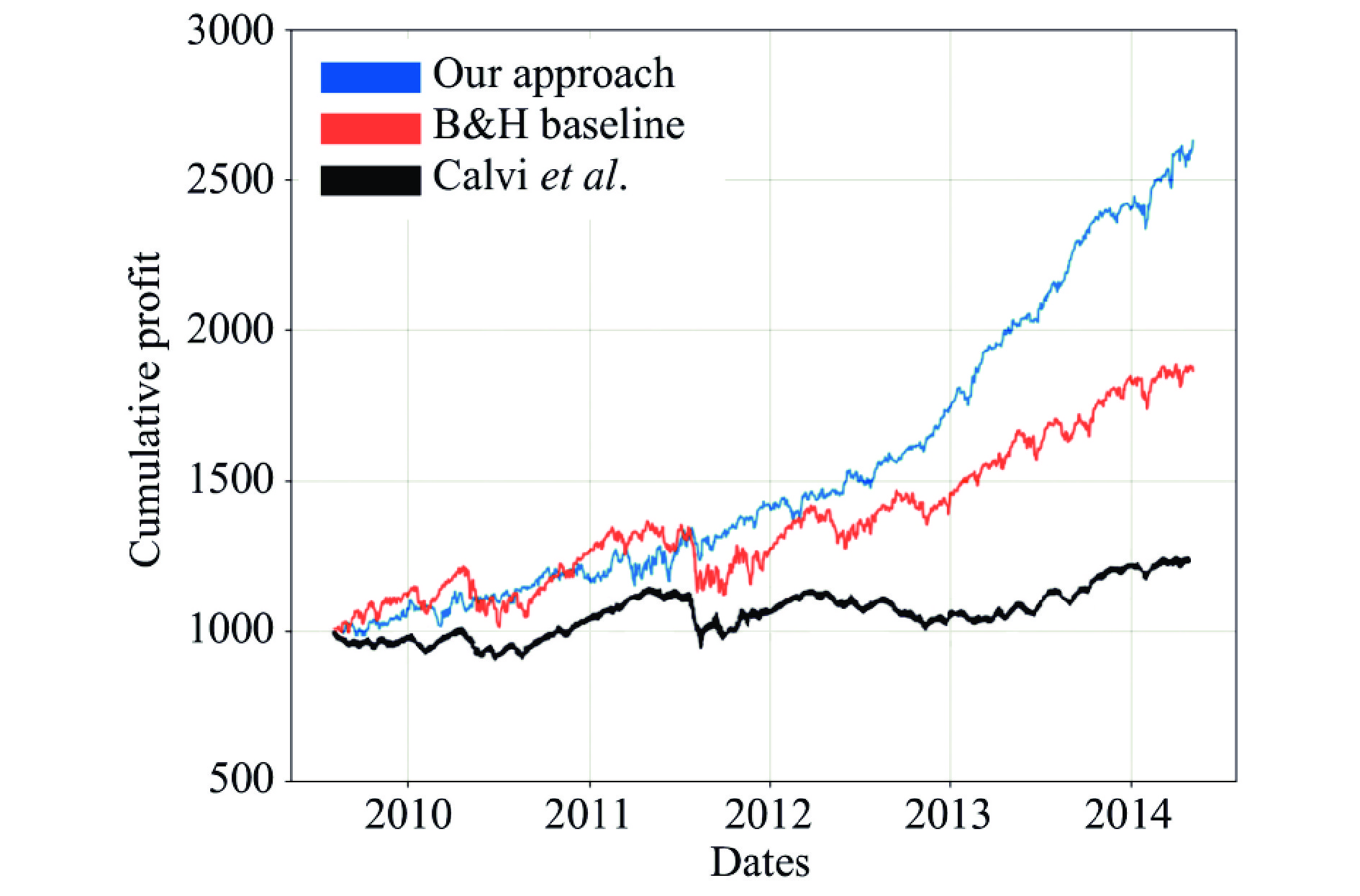

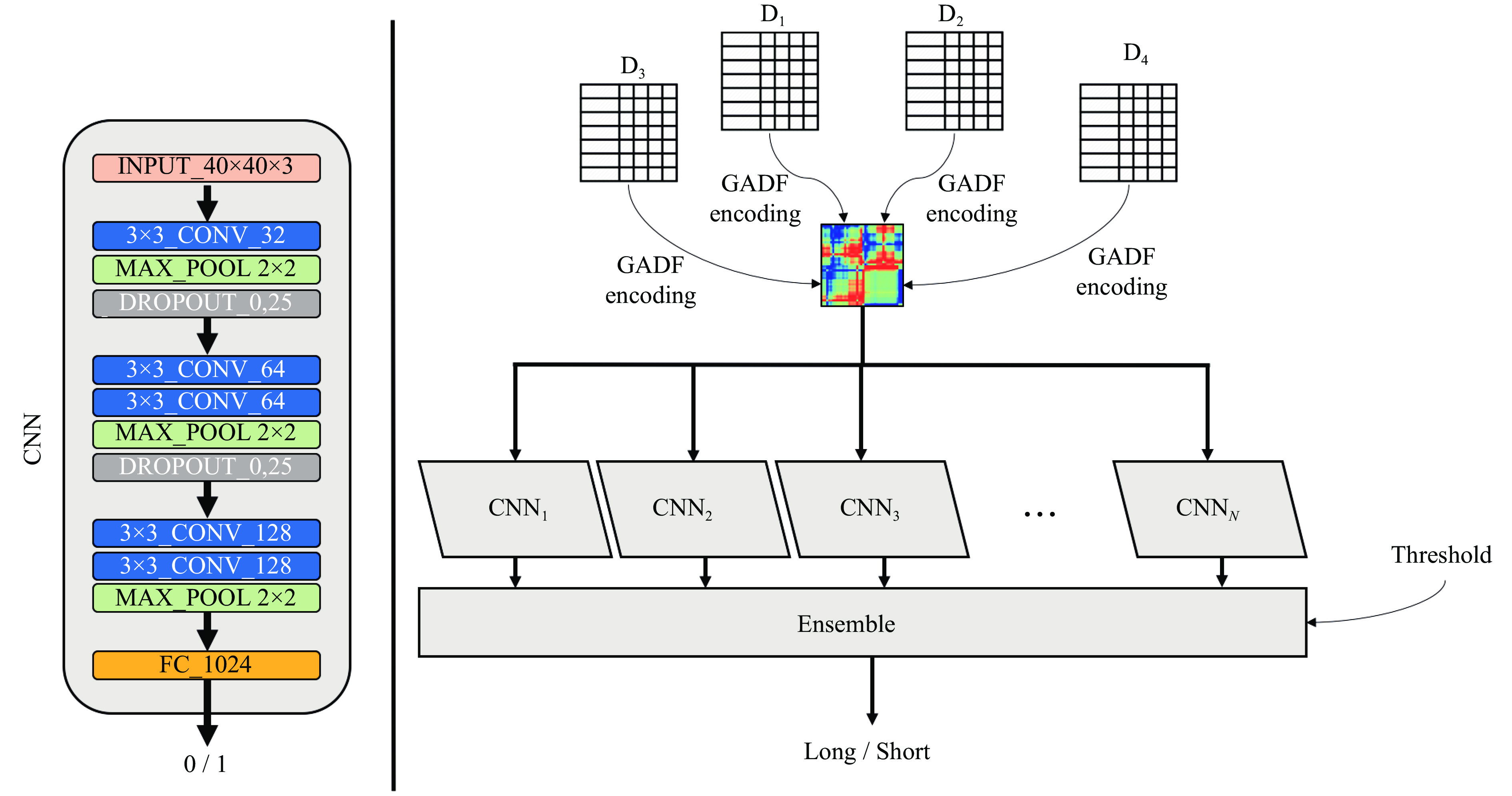

| Citation: | Silvio Barra, Salvatore Mario Carta, Andrea Corriga, Alessandro Sebastian Podda and Diego Reforgiato Recupero, "Deep Learning and Time Series-to-Image Encoding for Financial Forecasting," IEEE/CAA J. Autom. Sinica, vol. 7, no. 3, pp. 683-693, May 2020. doi: 10.1109/JAS.2020.1003132

|

| [1] |

T. Kimoto, K. Asakawa, M. Yoda, and M. Takeoka, “Stock market prediction system with modular neural networks,” in Proc. Int. Joint Conf. Neural Networks, San Diego, CA, USA, 1990, pp. 1–6.

|

| [2] |

Y. D. Zhang and L. E. Wu, “Stock market prediction of S&P500 via combination of improved BCO approach and BP neural network,” Expert Syst. Appl., vol. 36, no. 5, pp. 8849–8854, Jul. 2009. doi: 10.1016/j.eswa.2008.11.028

|

| [3] |

T. Z. Tan, C. Quek, and G. S. Ng, “Brain-inspired genetic complementary learning for stock market prediction,” in Proc. IEEE Congr. Evolutionary Computation, Edinburgh, Scotland, UK, 2005, pp. 2653–2660.

|

| [4] |

S. Soni, “Applications of ANNs in stock market prediction: a survey,” Int. J. Comput. Sci. Eng. Technol., vol. 2, no. 3, pp. 71–83, 2011.

|

| [5] |

T. Lintonen and T. Raty, “Self-learning of multivariate time series using perceptually important points,” IEEE/CAA J. Autom. Sinica, vol. 6, no. 6, pp. 1318–1331, Nov. 2019. doi: 10.1109/JAS.2019.1911777

|

| [6] |

K. Kamijo and T. Tanigawa, “Stock price pattern recognition-a recurrent neural network approach,” in Proc. Int. Joint Conf. Neural Networks, San Diego, CA, USA, 1990, pp. 215–221.

|

| [7] |

C. H. Lee and K. C. Park, “Prediction of monthly transition of the composition stock price index using recurrent back-propagation,” in Artificial Neural Networks, I. Aleksander and J. Taylor, Eds. Amsterdam, Netherlands: Elsevier, 1992, pp. 1629–1632.

|

| [8] |

E. Guresen, G. Kayakutlu, and T. U. Daim, “Using artificial neural network models in stock market index prediction,” Expert Syst. Appl., vol. 38, no. 8, pp. 10389–10397, Aug. 2011. doi: 10.1016/j.eswa.2011.02.068

|

| [9] |

S. C. Gao, M. C. Zhou, Y. R. Wang, J. J. Cheng, H. Yachi, and J. H. Wang, “Dendritic neuron model with effective learning algorithms for classification, approximation, and prediction,” IEEE Trans. Neural Netw. Learn. Syst., vol. 30, no. 2, pp. 601–614, Feb. 2019. doi: 10.1109/TNNLS.2018.2846646

|

| [10] |

D. B. Jia, S. X. Zheng, L. Yang, Y. Todo, and S. C. Gao, “A dendritic neuron model with nonlinearity validation on Istanbul stock and Taiwan futures exchange indexes prediction,” in Proc. 5th IEEE Int. Conf. Cloud Computing and Intelligence Systems, Nanjing, China, 2018, pp. 242–246.

|

| [11] |

T. L. Zhou, S. C. Gao, J. H. Wang, C. Y. Chu, Y. Todo, and Z. Tang, “Financial time series prediction using a dendritic neuron model,” Knowl-Based Syst., vol. 105, pp. 214–224, Aug. 2016. doi: 10.1016/j.knosys.2016.05.031

|

| [12] |

J. D. Farmer and A. W. Lo, “Frontiers of finance: evolution and efficient markets,” Proc. Natl. Acad. Sci. USA, vol. 96, no. 18, pp. 9991–9992, Aug. 1999. doi: 10.1073/pnas.96.18.9991

|

| [13] |

V. S. Pagolu, K. N. Reddy, G. Panda, and B. Majhi, “Sentiment analysis of twitter data for predicting stock market movements,” in Proc. Int. Conf. Signal Processing, Communication, Power and Embedded System, Paralakhemundi, India, 2016, pp. 1345–1350.

|

| [14] |

A. Mittal and A. Goel, “Stock prediction using twitter sentiment analysis,” 2012. [Online]. Available:http://cs229.stanford.edu/proj2011/GoelMittal-StockMarketPredictionUsingTwitterSentimentAnalysis.pdf

|

| [15] |

N. Oliveira, P. Cortez, and N. Areal, “The impact of microblogging data for stock market prediction: using twitter to predict returns, volatility, trading volume and survey sentiment indices,” Expert Syst. Appl., vol. 73, pp. 125–144, May 2017. doi: 10.1016/j.eswa.2016.12.036

|

| [16] |

T. B. Trafalis and H. Ince, “Support vector machine for regression and applications to financial forecasting,” in Proc. IEEE-INNS-ENNS Int. Joint Conf. Neural Networks 2000. Neural Computing: New Challenges and Perspectives for the New Millennium, Como, Italy, 2000, pp. 348–353.

|

| [17] |

C. Cortes and V. Vapnik, “Support-vector networks,” Mach. Learn., vol. 20, no. 3, pp. 273–297, Sept. 1995.

|

| [18] |

B. M. Henrique, V. A. Sobreiro, and H. Kimura, “Literature review: machine learning techniques applied to financial market prediction,” Expert Syst. Appl., vol. 124, pp. 226–251, Jun. 2019. doi: 10.1016/j.eswa.2019.01.012

|

| [19] |

C. F. Tsai and S. P. Wang, “Stock price forecasting by hybrid machine learning techniques,” in Proc. Int. MultiConf. Engineers and Computer Scientists, Hong Kong, China, 2009, pp. 60.

|

| [20] |

J. Patel, S. Shah, P. Thakkar, and K. Kotecha, “Predicting stock market index using fusion of machine learning techniques,” Expert Syst. Appl., vol. 42, no. 4, pp. 2162–2172, Mar. 2015. doi: 10.1016/j.eswa.2014.10.031

|

| [21] |

D. Shah, H. Isah, and F. Zulkernine, “Stock market analysis: a review and taxonomy of prediction techniques,” Int. J. Financ. Stud., vol. 7, no. 2, pp. 26, Jun. 2019. doi: 10.3390/ijfs7020026

|

| [22] |

M. Ballings, D. van den Poel, N. Hespeels, and R. Gryp, “Evaluating multiple classifiers for stock price direction prediction,” Expert Syst. Appl., vol. 42, no. 20, pp. 7046–7056, Nov. 2015. doi: 10.1016/j.eswa.2015.05.013

|

| [23] |

S. Basak, S. Kar, S. Saha, L. Khaidem, and S. R. Dey, “Predicting the direction of stock market prices using tree-based classifiers,” North Am. J. Econ. Finance, vol. 47, pp. 552–567, Jan. 2019. doi: 10.1016/j.najef.2018.06.013

|

| [24] |

S. Dey, Y. Kumar, S. Saha, and S. Basak, “Forecasting to classification: predicting the direction of stock market price using Xtreme gradient boosting,” 2016. [Online]. Available: https://doi.org/10.13140/RG.2.2.15294.48968

|

| [25] |

S. K. Aggarwal, L. M. Saini, and A. Kumar, “Price forecasting using wavelet transform and LSE based mixed model in Australian electricity market,” Int. J. Energy Sector Manage., vol. 2, no. 4, pp. 521–546, Nov. 2008. doi: 10.1108/17506220810919054

|

| [26] |

P. M. Kebria, A. Khosravi, S. M. Salaken, and S. Nahavandi, “Deep imitation learning for autonomous vehicles based on convolutional neural networks,” IEEE/CAA J. Autom. Sinica, vol. 7, no. 1, pp. 82–95, Jan. 2020. doi: 10.1109/JAS.2019.1911825

|

| [27] |

D. Freire-Obregón, F. Narducci, S. Barra, and M. Castrillón-Santana, “Deep learning for source camera identification on mobile devices,” Pattern Recognit. Lett., vol. 126, pp. 86–91, Sept. 2019. doi: 10.1016/j.patrec.2018.01.005

|

| [28] |

Z. G. Wang and T. Oates, “Imaging time-series to improve classification and imputation,” in Proc. 24th Int. Joint Conf. Artificial Intelligence, 2015.

|

| [29] |

G. G. Calvi, V. Lucic, and D. P. Mandic, “Support tensor machine for financial forecasting,” in Proc. IEEE Int. Conf. Acoustics, Speech and Signal Processing, Brighton, United Kingdom, 2019, pp. 8152–8156.

|

| [30] |

Z. G. Wang and T. Oates, “Encoding time series as images for visual inspection and classification using tiled convolutional neural networks,” in Proc. Workshops at the 29th AAAI Conf. Artificial Intelligence, 2015.

|

| [31] |

K. Simonyan and A. Zisserman, “Very deep convolutional networks for large-scale image recognition,” arXiv: 1409.1556, 2014.

|

| [32] |

K. M. He, X. Y. Zhang, S. Q. Ren, and J. Sun, “Deep residual learning for image recognition,” in Proc. IEEE Conf. Computer Vision and Pattern Recognition, Las Vegas, NV, USA, 2016, pp. 770–778.

|

| [33] |

P. Cizeau, Y. H. Liu, M. Meyer, C. K. Peng, and H. E. Stanley, “Volatility distribution in the S&P500 stock index,” Phys. A Stat. Mech. Appl., vol. 245, no. 3–4, pp. 441–445, Nov. 1997. doi: 10.1016/S0378-4371(97)00417-2

|

| [34] |

M. Martens, “Measuring and forecasting S&P500 index-futures volatility using high-frequency data,” J. Futur. Mark., vol. 22, no. 6, pp. 497–518, Jun. 2002. doi: 10.1002/fut.10016

|

Figures(6) / Tables(3)

DownLoad:

DownLoad: